Oops! We couldn’t find any results...

Oops! We couldn’t find any results...

What is inflation?

“In the simplest terms, inflation occurs when there's too much money in the system. On the flip side, deflation occurs when there are too few dollars in circulation.”

Robert Kiyosaki

Inflation refers to the general increase in the price of goods and services in an economy over time. When inflation is high, goods are more expensive and your dollar doesn't buy as much. This is due to purchasing power, which determines how far your dollar can go in a given economy. On the flip side, when inflation is low, each dollar has more purchasing power (so you can buy more).

How is the inflation rate measured?

The inflation rate is usually measured by a change in the price index. The Bureau of Labor and Statistics measures this index, called the Consumer Price Index (“CPI”). The CPI tracks the average change over time in a specific basket of goods and services.

This average is divided by the price of that same basket in the previous year, resulting in an inflationary increase or decrease.

What causes inflation?

Several factors contribute to inflation, but the main drivers are typically increases in the money supply, government spending, or both.

When the government prints more money than there is demand for, the value of each dollar decreases.

In the U.S., the Federal Reserve (the "Fed") controls the monetary system. The Fed attempts to balance inflation by manipulating interest rates, with an aim to keep the rate at or around 2%.

However, this is no easy task since several factors impact the cost of goods and services.

If inflation shoots up, the Fed might raise interest rates to bring it back down. If the inflationary rate drops too low, the Fed might lower interest rates to give the economy a jolt.

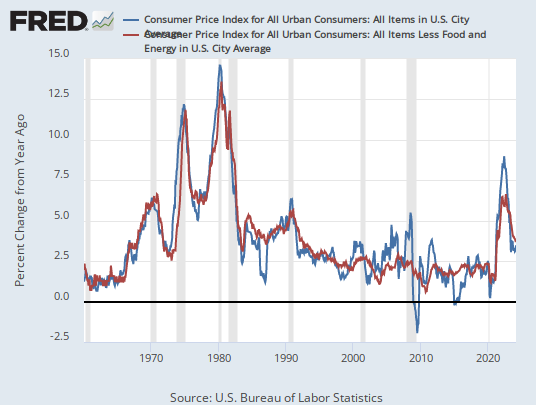

Historical inflation rates

The chart below shows the rate of inflation over the last 50+ years. As you can see, the 1970s were a time of extremely high inflation, followed by a gradual decline into 2020.

The trend started to reverse after the coronavirus upended global supply chains and disrupted labor markets. At the end of November 2021, the rate was 6.8%—the highest in three decades.

How does inflation affect your money?

Goods and services

Inflation is tied to the cost of goods and services that we purchase and use every day.

One recent example occurred during the pandemic when the average cost of new vehicles increased due to a shortage of microchips. Since microchips run the cars and there weren’t enough of them, the price of the cars also rose.

This is a prime example of how a breakdown in the supply chain can raise prices, causing a domino effect that impacts businesses and consumers alike.

Cash, savings, and investments

Cash: Over time, inflation can reduce the value of your money. For example, if you stash away $1,000 under your mattress today and then go to spend it twenty years from now, that cash may not be able to buy as much. So while you won't actually lose any money, your purchasing power is weakened by the rise in goods and services.

Savings: If you have money in the bank, the interest you earn may help balance some of the inflation effects. However, your savings may not grow fast enough to offset the inflation loss completely.

Investments: The impact of inflation on investments varies by class. For some assets, like regular bonds and certificates of deposit, inflation can hurt performance since your interest payment remains the same throughout the term of the contract.

The effect on stocks varies by type as well. For example, sometimes inflation is high when the economy is strong. During these times, consumers tend to buy more things. In this case, a company's share price might rise because its revenue is increasing.

On the other hand, sometimes companies might raise wages and prices for raw materials, making it harder to sell their goods. This could put a damper on their share price.

Borrowing power

High levels of inflation can also lead to the government raising interest rates. When this happens, borrowers have a harder time affording the extra cost (interest) to borrow money from the banks for big-ticket items like homes, cars, and furniture.

How can I combat the effects of inflation on my investments?

Investors can employ a few strategies when trying to hedge against inflation, but it’s important to note that they have varying degrees of success. To that end, there is no one-size-fits-all plan (everyone has different investment objectives).

Here are a few types of investments that investors use to counter a higher cost of living.

Commodities such as gold or silver are often seen as a hedge against inflation because their prices usually increase when inflation rises.

Equities (i.e., individual stocks, mutual funds, and ETFs) typically outpace inflation in the long run, so allocating a certain amount of your assets to this bucket is always a sound choice.

Crypto doesn’t have a long enough history to be declared a bona fide hedge to inflation. However, that hasn’t stopped billionaire investors like Paul Tudor Jones from touting Bitcoin as “a great way to protect wealth over the long run,” calling it “a store of wealth like gold.”

Inflation is a complicated issue. So, it’s important to note that the effects on an individual can, at times, be positive—but, it all depends on their situation.

For example, as prices rise due to increased demand, businesses may need to hire more workers, which could lead to higher wages if salaries are tied to inflation rates. In addition, government benefits (i.e., Social Security) might also be adjusted with cost-of-living increases, further helping recipients to keep costs low and boost spending power.

The reality is, you can’t control inflation, but that doesn't mean you have to let it get in the way of your financial goals. With a bit of planning and smart money management skills, you'll be able to keep your objectives on track without skipping a beat.

1 comment